How to Pay for College in 2026: FAFSA, Grants, Scholarships, Loans, and Smart Money Strategies

Learn how to pay for college with FAFSA, Pell Grants, scholarships, state aid, work-study, 529 plans, tax credits, and smart borrowing. A complete 2026 guide for high school seniors.

How to Pay for College

Paying for college is not usually one big payment from one source. For most students, it is a stack: federal aid, state aid, school aid, scholarships, savings, work-study, tax benefits, and sometimes student loans. That matters because the average 2025–26 published tuition and fees are about $4,150 at public two-year colleges, $11,950 for in-state students at public four-year colleges, and $45,000 at private nonprofit four-year colleges. Total average student budgets are much higher once housing, food, books, transportation, and other expenses are included. At the same time, the majority of full-time undergraduates receive grant aid, and average aid per full-time-equivalent undergraduate student in 2024–25 was $16,810.

The big idea is simple: pay for college in this order—free money first, lower-cost and tax-advantaged options second, federal loans third, and private loans last. That order reduces risk and usually cuts what you pay out of pocket over four years.

The first thing every senior should do

If you are going to college, career school, or trade school for the 2026–27 academic year, the 2026–27 FAFSA is now available and covers attendance between July 1, 2026 and June 30, 2027. Completing the FAFSA is free and is the starting point for federal grants, work-study, and federal student loans. States, colleges, and some private aid providers also use FAFSA data, so filing early matters even if you are not sure you will qualify.

On the current FAFSA, students are encouraged to start their own form first. Dependent students usually need at least one parent contributor, and each contributor needs their own StudentAid.gov account. Federal Student Aid says most people can complete the FAFSA in less than 30 minutes, including gathering basic information.

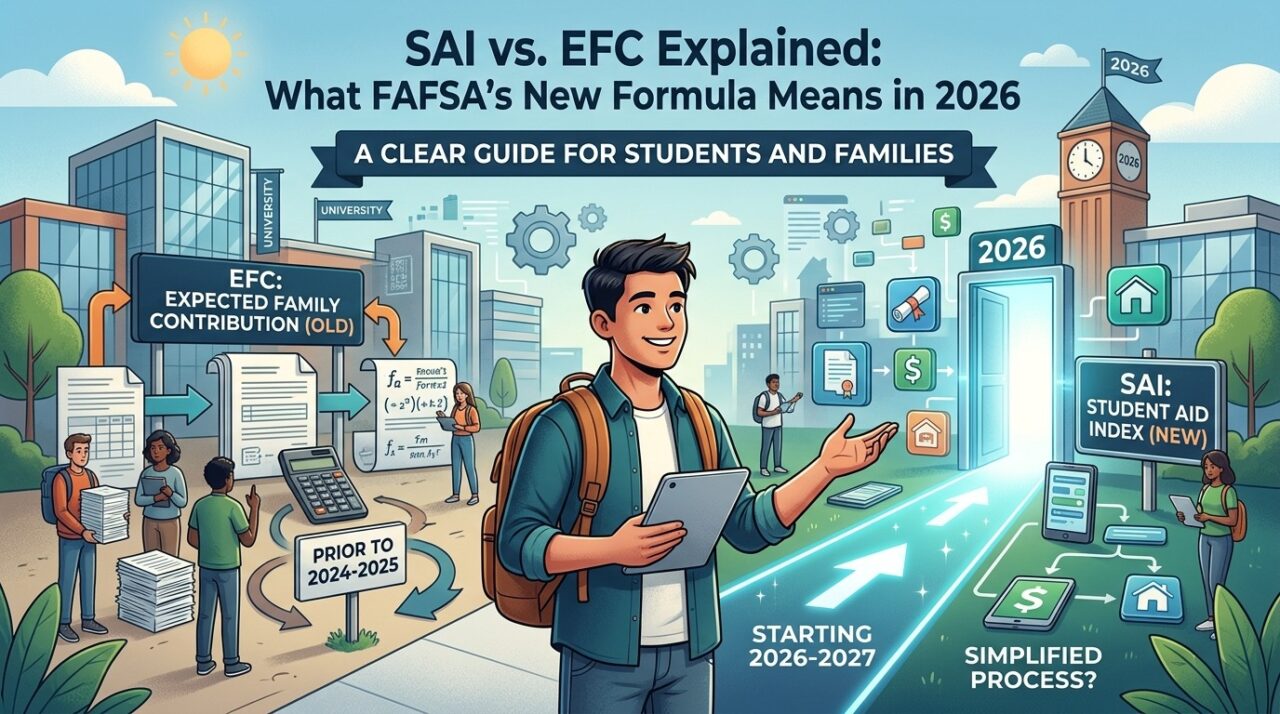

A key FAFSA term is the Student Aid Index (SAI). The SAI ranges from –1500 to 999999. It is not a bill, not the amount your family must pay, and not your final aid offer. It is an index schools use to help determine need-based aid, including Pell Grant eligibility. Lower SAI numbers generally signal higher financial need.

What college really costs: sticker price vs. net price

One of the biggest mistakes students make is focusing only on sticker price. A college that looks more expensive can end up costing less after grants and scholarships. Federal Student Aid recommends comparing net price, not published price. Net price is the total cost of attendance minus grants and scholarships that do not have to be repaid.

That is especially important because average full-year student budgets in 2025–26 are estimated at about $21,320 for public two-year in-district students, $30,990 for public four-year in-state students, $50,920 for public four-year out-of-state students, and $65,470 for private nonprofit four-year students. Those figures include more than tuition: housing, food, books, transportation, and other expenses matter too.

Before you apply—or at least before you commit—use each school’s net price calculator and compare schools in College Scorecard. NCES says net price calculators are required for Title IV colleges that enroll first-time, full-time undergraduates, and Federal Student Aid recommends College Scorecard for comparing average costs, net prices, graduation rates, earnings, and debt.

The best way to pay for college: build your aid stack

1) Federal grants: start with money you do not repay

For many families, the most important federal grant is the Pell Grant. For the 2026–27 award year, the maximum Pell Grant is $7,395. Some students can also receive up to 150% of their annual Pell award through “year-round Pell” if they attend an additional term in the same school year. Pell does not have to be repaid except in limited circumstances.

There are other federal grants too. The Federal Supplemental Educational Opportunity Grant (FSEOG) is for undergraduates with exceptional financial need and is awarded by participating schools, with Pell recipients getting priority. Federal Student Aid materials also show FSEOG awards can be up to $4,000, but funding is limited by campus allocations, so early FAFSA filing helps.

If you plan to become a teacher in a high-need field, the TEACH Grant can provide up to $4,000 per year, but it comes with a service obligation. If you do not complete the required teaching service, the grant can convert into a Direct Unsubsidized Loan.

2) State aid: do not stop after the FAFSA

Federal Student Aid is clear that student aid does not come only from Washington or from your college. States offer their own grants and scholarships, and some states require a separate state aid application in addition to the FAFSA. Many state programs are first-come, first-served or limited by annual appropriations, so early action matters.

To find the right state office, use the U.S. Department of Education’s state higher education agency directory. For example, New York’s state higher education agency is HESC, listed directly on the Department of Education’s state contacts page.

3) Institutional aid: college money can be a game changer

A school’s own grants and scholarships can dramatically change affordability. Federal Student Aid notes that institutional aid may be based on financial need, merit, academics, specialized majors, athletics, or other priorities, and it can lower out-of-pocket cost so much that a higher-priced school becomes the cheaper option. That is why offer letters should be compared using net price, not brand name or sticker price.

This is also why some public two-year colleges can be surprisingly affordable. College Board reports that, on average, first-time full-time students at public two-year colleges have been receiving enough grant aid to cover tuition and fees since 2009–10.

4) Scholarships: free money that fills the gap

Scholarships are still one of the best ways to close the gap between what a school costs and what your aid offer covers. Federal Student Aid specifically recommends applying for scholarships before your aid offers arrive because many deadlines come early.

A real rule to remember: you should not have to pay to file the FAFSA or to search for legitimate scholarships. Federal Student Aid warns students to avoid scams and to stick to trusted sources.

5) Work-study: useful, but not the same as a grant

Federal Work-Study can help students earn money through a job, often with scheduling built around school. But it is not the same as a grant that automatically reduces your bill on day one. You need to be awarded work-study, get a job, and work the hours to earn the money. Federal Student Aid notes that your earnings cannot exceed your work-study award amount.

When you compare aid offers, treat work-study as potential earnings, not guaranteed upfront cash. That mindset prevents students from underestimating what they will actually need before the semester begins.

6) 529 plans and family savings: tax-advantaged money still matters

A 529 plan—formally a qualified tuition program—is a state-sponsored education savings vehicle. The IRS says earnings grow tax-free, and distributions are generally not taxable when used for qualified higher education expenses.

For families who already have a 529, that money often belongs near the front of the pay-for-college stack because it can reduce borrowing. The IRS also notes that limited student loan repayment from a 529 is allowed, but the core use case for most families remains paying qualified college expenses directly.

7) Tax credits can lower the real cost after enrollment

Tax benefits do not usually help with the first tuition bill in real time, but they can lower the total cost of college over the year. The American Opportunity Tax Credit (AOTC) can be worth up to $2,500 per eligible student per year for the first four years of higher education, and up to 40% of the remaining credit can be refundable, up to $1,000.

The Lifetime Learning Credit (LLC) can be worth up to $2,000 per return and is useful in situations where the AOTC does not apply. The IRS also makes clear that you cannot double-count the same student and same expenses for both credits.

8) Employer education benefits can help some students and families

If you work while in school—or if a parent is deciding whether to switch jobs or stay with an employer—education benefits are worth checking. The IRS says employer-provided educational assistance can be excluded from wages up to $5,250 per year, and qualifying programs can cover tuition, fees, books, supplies, equipment, and in some cases student loan payments.

For adult learners this can be a major funding source, but even for traditional students it matters because family financial decisions often affect how much borrowing will be needed.

9) Military and veteran education benefits can cover major costs

For eligible military-connected students and families, VA education benefits can cover all or part of school and training costs. The Department of Veterans Affairs says GI Bill benefits help qualifying veterans and family members pay for school and related expenses, and VA also offers tools such as the GI Bill Comparison Tool and information about the Yellow Ribbon Program.

If you or a parent has military service, this should be reviewed early because it can change the whole financing plan.

10) Federal student loans: borrow carefully, but use them before private loans

If free money and savings do not cover the full cost, federal student loans are usually the next best option. For dependent undergraduates, current annual borrowing limits are $5,500 for first year, $6,500 for second year, and $7,500 for third year and beyond, with a $31,000 total undergraduate limit. Independent students can borrow more.

For loans first disbursed between July 1, 2025 and June 30, 2026, the interest rate for undergraduate Direct Subsidized and Direct Unsubsidized Loans is 6.39%. Direct PLUS Loans for parents and graduate students are 8.94% for that same period.

Subsidized loans are better when you qualify because the government pays the interest while you are in school at least half time and during certain other periods. Unsubsidized loans start accruing interest earlier.

Parent PLUS Loans can help families bridge a gap, but they require a credit check, and the borrower cannot have an adverse credit history unless other requirements are met. That makes them more expensive and riskier than standard undergraduate Direct Loans.

Private student loans should be the last resort

If you must borrow, federal loans usually come before private loans. The CFPB says federal student loans are the best option for the vast majority of borrowers because they have fixed interest rates and stronger protections. Federal Student Aid also notes that private loans often require a credit record or cosigner and may have fewer protections if repayment becomes difficult.

That does not mean private loans are never used. It means they should usually come after grants, scholarships, school aid, work-study, 529 money, tax benefits, and available federal loans.

A smart step-by-step plan for high school seniors

Start by making a college list that includes at least one school you know is likely affordable. Then run each school’s net price calculator and compare results in College Scorecard so you understand likely out-of-pocket cost before emotions take over.

Next, complete the FAFSA as early as possible and make sure every required contributor finishes their section and signs. If any school on your list requires the CSS Profile, complete that too. College Board says the CSS Profile unlocks access to more than $14 billion in nonfederal aid each year.

Then apply for state aid and scholarships at the same time. Federal Student Aid explicitly recommends continuing scholarship applications while you wait for aid offers.

When aid offers arrive, compare them by asking four questions:

How much is free money? How much is earned money? How much is borrowed money? What is my net price? Federal Student Aid’s formula is straightforward: total cost minus grants and scholarships equals your net price.

Finally, borrow only what you truly need. If you already know your likely debt, use the federal Loan Simulator to estimate future monthly payments before you sign.

Common mistakes to avoid

Do not skip the FAFSA because you think your family income is too high. Pell is only one part of the system, and FAFSA data is also used for other federal, state, school, and private aid programs.

Do not wait until the federal deadline. The federal FAFSA deadline can run as late as June 30, but state and school money may run out earlier.

Do not compare schools by sticker price alone. Compare net price.

Do not treat work-study like guaranteed bill reduction. You earn it through a job.

Do not jump to private loans before you understand federal loans and all other options.

Official websites to use

Final takeaway

The best way to pay for college is usually not “find one thing that covers everything.” It is building the right stack in the right order: FAFSA first, grants and scholarships next, state and school aid after that, savings and tax benefits where available, federal loans only as needed, and private loans last. Students who understand net price, file early, and compare aid offers carefully usually make stronger college decisions than students who chase the lowest sticker price or the biggest school name.