How Does Paying for College Work?

Paying for college does not usually happen with one single check from one single source. In real life, most students pay with a mix of grants, scholarships, federal aid, family savings or income, part-time work, and sometimes loans. The FAFSA is the starting point for most of that system because states, colleges, and the federal government use it to decide what aid you can receive.

The easiest way to understand college payment is this:

Cost of attendance

minus grants and scholarships

minus family savings, 529 money, tax benefits, and monthly payments

minus work income

equals the gap you still need to cover

That remaining gap is where federal student loans, Parent PLUS loans, or private loans may enter the picture. The smartest families try to fill that gap in the cheapest order first: free money first, borrowing last.

The first thing to know: sticker price is not the real price

A lot of families look at a college’s posted tuition and panic. That number matters, but it is not the full story and it is often not the final amount a family pays.

The government and colleges use a larger number called cost of attendance (COA). COA includes more than tuition. It can include tuition and fees, books and supplies, room and board, transportation, and other expenses. NCES also defines net price as the actual amount students and families need to cover after subtracting grant and scholarship aid from the total cost.

Here is what the official national data looked like most recently:

At 4-year colleges in 2022–23, average tuition and fees were about $9,800 at public institutions and $40,700 at private nonprofit institutions. At 2-year colleges, average tuition and fees were about $4,000 at public institutions.

Living arrangement changes the total bill a lot. In 2022–23, the average total cost of attendance for first-time, full-time undergraduates at public 4-year institutions was about $27,100 living on campus, $27,800 off campus not with family, and $15,700 off campus with family. At public 2-year institutions, it was about $16,600 on campus, $20,900 off campus not with family, and $10,200 off campus with family.

That is why families should focus on net price, not just sticker price. In 2021–22, the average net price for aid recipients was about $15,200 at public 4-year colleges, $8,300 at public 2-year colleges, and $29,700 at private nonprofit 4-year colleges.

Step 1: Complete the FAFSA

For most students, college payment starts with the FAFSA. The FAFSA is free, and for the 2026–27 school year, federal guidance says to submit it as early as possible, but no earlier than October 1, 2025. State and college deadlines can be earlier or more competitive, so waiting can cost you aid.

The FAFSA is not only for federal aid. The Department of Education says schools, states, and some private aid providers also use FAFSA data to award their own aid. The current student instructions for the 2026–27 form say it takes most people less than 30 minutes to complete.

If you are a dependent student, you usually must include parent information. The FAFSA now uses a contributor system, and each contributor needs their own StudentAid.gov account to complete and sign their section. For 2026–27, the form uses 2024 tax information, and contributors must provide consent for federal tax data transfer; if required consent is not provided, the student is not eligible for federal aid.

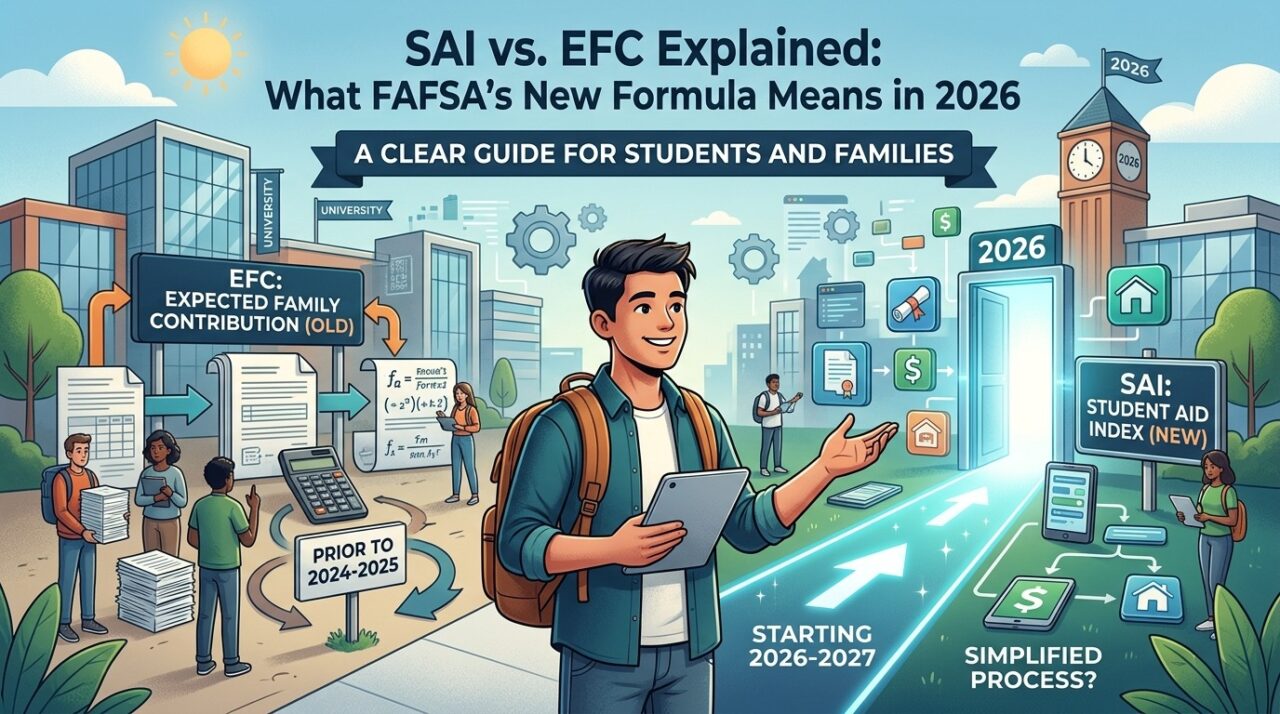

Step 2: Understand what the Student Aid Index means

After the FAFSA is processed, you receive a FAFSA Submission Summary. Federal Student Aid says this usually takes one to three business days after you submit a completed form online.

One of the most misunderstood numbers on that summary is the Student Aid Index, or SAI. The SAI is a formula-based index number ranging from –1500 to 999999. It is not the amount of aid you will get, not your actual bill, and not the amount your family is expected to pay. Schools use it, together with cost of attendance, to build your aid offer. Lower or negative SAI values generally indicate higher financial need and a higher likelihood of Pell Grant eligibility.

Step 3: Read your aid offer in the right order

When an aid offer arrives, do not just look at the big total. Break it into categories.

1) Grants and scholarships

This is the best money because it usually does not have to be repaid. The biggest federal grant is the Pell Grant. For the 2026–27 award year, the maximum Pell Grant is $7,395. Federal Student Aid also says some students can receive up to 150% of their yearly Pell award through year-round Pell if they attend an additional term, and Pell eligibility generally lasts for about six years total.

Scholarships also reduce what you need to pay, but there is an important rule: your total aid package cannot exceed the school’s cost of attendance, so an outside scholarship can sometimes change how the rest of your aid is arranged.

2) Work-study

Federal Work-Study is not a discount on your bill up front. It is a way to earn money through a part-time job while you are enrolled. Federal Student Aid says Work-Study provides part-time jobs for students with financial need and is designed to help students gain work experience while paying for school.

3) Federal student loans

Federal student loans matter because they usually come with more borrower protections than private loans.

For dependent undergraduates, current federal annual limits are:

-

First year: $5,500 total, up to $3,500 subsidized

-

Second year: $6,500 total, up to $4,500 subsidized

-

Third year and beyond: $7,500 total, up to $5,500 subsidized

For independent undergraduates or certain dependent students whose parents cannot get PLUS loans, the annual limits are higher:

-

First year: $9,500

-

Second year: $10,500

-

Third year and beyond: $12,500

A subsidized loan is better than an unsubsidized loan because the government covers interest in certain periods while you are in school if you qualify. With unsubsidized loans, interest grows while you are enrolled.

For loans first disbursed from July 1, 2025 through June 30, 2026, the fixed interest rate is 6.39% for undergraduate Direct Subsidized and Unsubsidized Loans, and 8.94% for Parent PLUS and Grad PLUS Loans. These rates are reset annually, so rates for loans first disbursed on or after July 1, 2026 will be published separately.

4) Family money, 529 money, and tax benefits

Families also pay for college through checking and savings, current income, 529 plans, and tax credits.

The IRS says a 529 plan is a state-run qualified tuition program that lets families save for qualified education expenses. Qualified higher education expenses generally include costs required for enrollment or attendance at eligible postsecondary institutions, and the IRS says earnings are generally tax-free when used for qualified expenses.

The American Opportunity Tax Credit can also matter. The IRS says eligible families can receive up to $2,500 per student per year for the first four years of higher education, and up to 40% of the remaining credit, or $1,000, can be refundable if the credit reduces tax owed to zero.

5) Tuition payment plans

Many colleges let families split the semester bill into monthly installments. The CFPB says tuition payment plans are short-term plans that divide college bills into equal monthly payments. They are usually interest-free, but many plans charge enrollment fees, late fees, or returned payment fees.

6) Parent PLUS loans and private loans

If free aid, work, and federal student loans still do not close the gap, some families look at Parent PLUS or private loans.

A Parent PLUS Loan is borrowed by the parent, not the student. The parent can generally borrow up to the cost of education minus other financial aid received. Federal materials also explain that repayment usually begins right after the final disbursement, although deferment may be available while the student is enrolled at least half-time and for an additional six months afterward.

Private loans are usually the last resort. Federal Student Aid recommends federal aid first and warns that private loans may require a cosigner and may offer fewer protections such as deferment, forbearance, flexible repayment, or forgiveness options.

Step 4: Compare colleges by net price, not emotion

A smart college choice is not just “Where did I get in?” It is also “Which school gives me the best outcome for the lowest realistic cost?”

Federal Student Aid advises students to compare aid offers carefully and to include unexpected costs that may not be fully reflected in a school’s cost of attendance. That matters because books, travel, and personal expenses are real costs even when families forget to budget for them.

A better comparison method looks like this:

School A total cost of attendance

minus gift aid

minus family contribution from savings/current income/529

minus payment plan amount you can actually afford

equals remaining gap

Do that for every school. Then ask one more question: How much debt will I need over four years, not just year one? That is where the federal Net Price Calculator, College Navigator, and College Scorecard become useful. NCES says net price calculators are required for many Title IV schools and are meant to estimate net price based on what similar students paid. College Scorecard lets students compare schools, fields of study, salaries, and debt.

Step 5: Know how colleges actually receive and apply the money

Aid usually does not arrive as cash in your hand first.

Federal student loan documents explain that schools generally disburse loan funds in more than one installment, often by term. In most cases, the school first applies the money to your school account for tuition, room and board, and authorized fees. If money is left over, that is called a credit balance. Unless you authorize the school to hold it, the school generally must send that balance to you within 14 days after the balance occurs or 14 days after classes begin, whichever is later.

That leftover money is not free spending money. Federal loan rules say loan funds may be used only for authorized educational expenses, including tuition, room, board, books, supplies, equipment, transportation, commuting costs, and certain other documented education costs.

Step 6: You can reduce borrowing after you accept it

Many students do not realize that a loan offer is not an all-or-nothing decision. You can often borrow less than the maximum offered.

Federal loan documents say you may cancel all or part of a federal loan before disbursement, and after disbursement you may still cancel or return all or part of it within certain timeframes. If you return the amount within 120 days of disbursement, you generally do not have to pay the interest or loan fee on the returned portion.

That matters because many students accept the full loan amount automatically, then discover later that they did not actually need all of it.

Step 7: Paying for college is a yearly process, not a one-time event

One of the biggest mistakes families make is treating college financing like a one-time event senior year. It is not. You normally need to file the FAFSA every year you are enrolled if you want federal aid, and schools can change your package from year to year based on income, cost changes, or school policy.

That means the best college decision is not just “Can we pay freshman year?” It is “Can we pay all the way to graduation without dangerous debt?”

The smartest payment order for most students

For most families, the healthiest order looks like this:

-

Apply for FAFSA-based aid early

-

Take grants and scholarships first

-

Use savings/current income/529 funds

-

Use a low-fee monthly payment plan if needed

-

Use Federal Work-Study or a part-time job for ongoing expenses

-

Use federal student loans carefully

-

Use Parent PLUS or private loans only if the remaining gap is still manageable

Official links to legit websites

Use these in your WordPress post as trusted resources:

Final takeaway

How paying for college works is actually simple once you strip away the jargon:

Colleges start with total cost.

The FAFSA helps determine aid eligibility.

Schools build an offer using grants, scholarships, work-study, and loans.

Families cover the rest with savings, payment plans, tax benefits, work income, and only then borrowing if needed.

The students who usually make the strongest financial decision are not the ones who chase the biggest scholarship headline. They are the ones who compare net price, total four-year debt, and graduation value before they commit.